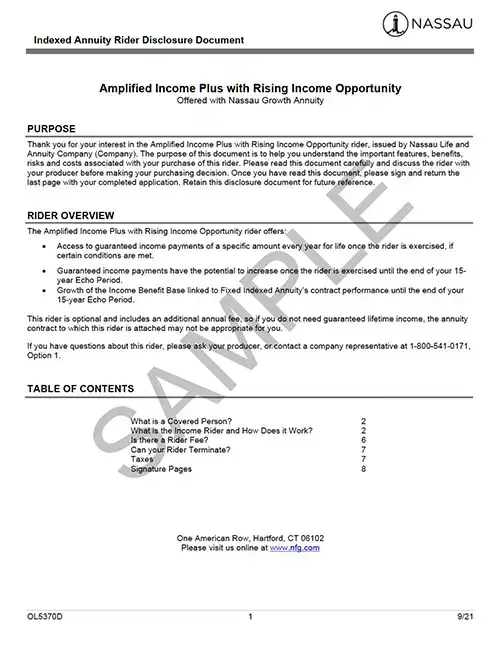

Nassau Growth Annuity®

Product Overview

Snapshot

Portfolio Position

Nassau Growth Annuity offers powerful growth potential and options for generating future income.

Consumer Description

Nassau Growth Annuity is a single premium accumulation-focused fixed indexed annuity with guaranteed lifetime withdrawal benefit options. It can help contract holders accumulate money by leveraging several indexed accounts which earn interest based on the positive performance of one of three indices, all while protecting the growth from market losses.

Riders

Nassau Growth Annuity can help individuals build on their contract growth for their future income needs. The Amplified Income, Amplified Income with Rising Income Opportunity (RIO), Amplified Income Plus, or Amplified Income Plus with RIO riders* include features to potentially boost income payments. Riders are only available for 10 year surrender charge schedule contracts (9 years in CA).

*Future income provided by these riders is dependent on the annuity's performance. An income rider is required to be elected at the time of application. Amplified Income Plus and Amplified Income Plus with RIO include an annual fee.

Marketing Materials*

Producer and Consumer Videos

Showing 1 of 2:

Contract Details

Rider Disclosure

Other Documents

Income Rider Annual Benefit Amount Supplement

Smart Passage SG Indexed Account Overview

Not for use in Idaho.

Important Disclosures

*Marketing materials are not approved for use in Idaho and Illinois. Contact the sales desk at 1-888-794-4447 for assets in these states.

We reserve the right to revise declared rates at any time.

For Producer Use Only. Not for distribution to the public.

Product features, rider options, and availability may vary by state. Riders unavailable to Covered Persons under age 50 in Maryland. Product sales must be appropriate based on a comprehensive evaluation of the customer's financial situation, needs, and objectives. Guarantees are based on the claims-paying ability of the issuing company. Nassau does not provide financial, investment or tax advice or act as a fiduciary in the sale or service of its products.

Annuities are long-term products particularly suitable for retirement assets. Annuities held within qualified plans do not provide any additional tax benefit. Early withdrawals may be subject to surrender charges. Withdrawals are subject to ordinary income tax, and if taken prior to age 59½, a 10% IRS penalty may also apply.

Interest rates, participation rates, spread rates, caps and strategy fees are subject to change. All indexed account credit calculations exclude dividends. While the value of each indexed account is affected by the value of an outside index, the contract does not directly participate in any stock, bond or equity investment. Dividend payments and distributions are not received from any index or component of any index. Nassau may change, add or eliminate indexed accounts. Certain accounts may not be available in all states. Although index credits are never less than 0%, it is possible for the contract to lose value if index credits are less than rider and strategy fees. Riders may involve an added fee that is deducted from the contract value. Terminal illness and nursing home waivers are only available for issue ages 80 and below. Nursing home waiver not available in CA.

Non-Security Status Disclosure –The Contract is not a Security. The Contract is not registered under the Securities Act of 1933 and is being offered and sold in reliance on an exemption therein.

Nasdaq® is a registered trademark of Nasdaq, Inc. (which with its affiliates is referred to as the “Corporations”) and are licensed for use by Nassau. The Product(s) have not been passed on by the Corporations as to their legality or suitability. The Product(s) are not issued, endorsed, sold, or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE PRODUCT(S).

The “S&P 500 Index” is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”) and has been licensed for use by Nassau Life and Annuity Company and its affiliates (collectively, “Nassau”). Standard & Poor’s®, S&P 500® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”) and these trademarks have been licensed and sublicensed for use by SPDJI and Nassau, respectively. Nassau products are not sponsored, endorsed, sold or promoted by SPDJI, S&P, or their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such products nor do they have any liability for any errors, omissions, or interruptions of the S&P 500 Index.

The Smart Passage SG Index (the “Index”) is the exclusive property of SG Americas Securities, LLC (SG Americas Securities, LLC, together with its affiliates, “SG”). SG has contracted with S&P Opco, LLC (a subsidiary of S&P Dow Jones Indices LLC) (“S&P”) to maintain and calculate the Index. “SG Americas Securities, LLC”, “SGAS”, “Société Générale”, “SG”, “Société Générale Indices”, “SGI”, and “Smart Passage SG Index” (collectively, the “SG Marks”) are trademarks or service marks of SG. SG has licensed use of the SG Marks to Nassau Life and Annuity Company (“NLA”) for use in a fixed indexed annuity offered by NLA (the “Fixed Indexed Annuity”). SG’s sole contractual relationship with NLA is to license the Index and the SG Marks to NLA. None of SG, S&P or other third party licensor (collectively, the “Index Parties”) to SG is acting, or has been authorized to act, as an agent of NLA or has in any way sponsored, promoted, solicited, negotiated, endorsed, offered, sold, issued, supported, structured or priced any Fixed Indexed Annuity or provided investment advice to NLA.

No Index Party has passed on the legality or suitability of, or the accuracy or adequacy of the descriptions and disclosures relating to, the Fixed Indexed Annuity, including those disclosures with respect to the Index. The Index Parties make no representation whatsoever, whether express or implied, as to the advisability of purchasing, selling or holding any product linked to the Index, including the Fixed Indexed Annuity, or the ability of the Index to meet its stated objectives, including meeting its target volatility. The Index Parties have no obligation to, and will not, take the needs of NLA or any annuitant into consideration in determining, composing or calculating the Index. The selection of the Index as a crediting option under a Fixed Indexed Annuity does not obligate NLA or SG to invest annuity payments in the components of the Index.

THE INDEX PARTIES MAKE NO REPRESENTATION OR WARRANTY WHATSOEVER, WHETHER EXPRESS OR IMPLIED, AND HEREBY EXPRESSLY DISCLAIM ALL WARRANTIES (INCLUDING, WITHOUT LIMITATION, THOSE OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE), WITH RESPECT TO THE INDEX OR ANY DATA INCLUDED THEREIN OR RELATING THERETO, AND IN PARTICULAR DISCLAIM ANY GUARANTEE OR WARRANTY EITHER AS TO THE QUALITY, ACCURACY, TIMELINESS AND/OR COMPLETENESS OF THE INDEX OR ANY DATA INCLUDED THEREIN, THE RESULTS OBTAINED FROM THE USE OF THE INDEX AND/OR THE CALCULATION OR COMPOSITION OF THE INDEX, OR CALCULATIONS MADE WITH RESPECT TO ANY FIXED INDEXED ANNUITY AT ANY PARTICULAR TIME ON ANY PARTICULAR DATE OR OTHERWISE. THE INDEX PARTIES SHALL NOT BE LIABLE (WHETHER IN NEGLIGENCE OR OTHERWISE) TO ANY PERSON FOR ANY ERROR OR OMISSION IN THE INDEX OR IN THE CALCULATION OF THE INDEX, AND THE INDEX PARTIES ARE UNDER NO OBLIGATION TO ADVISE ANY PERSON OF ANY ERROR THEREIN, OR FOR ANY INTERRUPTION IN THE CALCULATION OF THE INDEX. NO INDEX PARTY SHALL HAVE ANY LIABILITY TO ANY PARTY FOR ANY ACT OR FAILURE TO ACT BY THE INDEX PARTIES IN CONNECTION WITH THE DETERMINATION, ADJUSTMENT OR MAINTENANCE OF THE INDEX. WITHOUT LIMITING THE FOREGOING, IN NO EVENT SHALL AN INDEX PARTY HAVE ANY LIABILITY FOR ANY DIRECT DAMAGES, LOST PROFITS OR SPECIAL, INCIDENTAL, PUNITIVE, INDIRECT OR CONSEQUENTIAL DAMAGES, EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

No Index Party is a fiduciary or agent of any purchaser, seller or holder of a Fixed Indexed Annuity. None of SG, S&P or any third party licensor shall have any liability with respect to the Fixed Indexed Annuity in which an interest crediting option is based is on the Index, nor for any loss relating to the Fixed Indexed Annuity, whether arising directly or indirectly from the use of the Index, its methodology, any SG Mark or otherwise. Obligations to make payments under the Fixed Indexed Annuities are solely the obligation of NLA

In calculating the performance of the Index, SG deducts a maintenance fee of 0.50% per annum on the level of the Index, and fixed transaction and replication costs, each calculated and deducted on a daily basis. Because the Index can experience potential leverage up to 350%, the maintenance fee may be as high as 1.75% per year. The transaction and replication costs cover, among other things, rebalancing and replication costs. The total amount of transaction and replication costs is not predictable and will depend on a number of factors, including the performance of the index underlying the Index, and market conditions, among other factors. These fees and costs will reduce the potential positive change in the Index and increase the potential negative change in the Index. While the volatility control applied by the Index may result in less fluctuation in rates of return as compared to indices without volatility controls, it may also reduce the overall rate of return as compared to products not subject to volatility controls.

The Smart Passage SG Index was launched in 2019. Any index performance shown in illustrations and hypothetical examples for periods prior to the index launch dates is based on historical backcasting using hypothetical data. Past performance is not indicative of future results.

Sunrise Smart Passage SG accounts measure the percentage change in the index after the best monthly return for each year in the segment is set to zero (“Sunrise Adjustment”). The participation rate declared at the segment’s start is then applied to determine the index credit. Higher participation rates are possible due to the Sunrise Adjustment, but this account may under perform other accounts if the growth is concentrated in one or two months.

Nassau Growth Annuity (19FIA3, ICC19FIA3N, 19GLWB3, ICC19GLWB3.1, ICC19ECH and 19ECH) is issued by Nassau Life and Annuity Company (Hartford, CT). In California, Nassau Life and Annuity Company does business as “Nassau Life and Annuity Insurance Company.” Nassau Life and Annuity Company is not authorized to conduct business in ME and NY, but that is subject to change. Nassau Life and Annuity Company is a subsidiary of Nassau Financial Group.

Insurance Products: NOT FDIC or NCUAA Insured | NO Bank or Credit Union Guarantee

Nassau Growth Annuity is an insurance contract, not an investment; it doesn't provide ownership of any stocks, bonds, index funds, or other securities.

BPD 40793

01-26

FOR PRODUCER USE ONLY